Additional paid-in capital (APIC), is an accounting term referring to money an investor pays above and beyond the par value price of a stock. Paid-in capital is the amount of capital “paid in” by investors during common or preferred stock issuances, including the par value of the shares themselves plus amounts in excess of par value. Paid-in capital represents the funds raised by the business through selling its equity and not from ongoing business operations. Knowing where a company is allocating its capital and how it finances those investments is critical information before making an investment decision. This will increase the total balance as the issuance of the new preferred shares will lead to an increase in the paid-in capital as excess value is being recorded.

paid-in capital in excess of par value – common stock

Get stock recommendations, portfolio guidance, and more from The Motley Fool’s premium services. Volatility profiles based on trailing-three-year calculations of the standard deviation of service investment returns. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Both of these items are included next to one another in the SE section of the balance sheet. It is a great way to generate cash for businesses without first laying down any collateral.

Stockholders’ Equity Outline

The par value of the issued stock goes to the common or preferred stock line, while the amount paid by investors above and beyond the par value goes to the additional paid-in capital line. Shareholder’s equity is a section that includes capital contributed to the company plus its retained earnings from all prior years in business. The term “additional paid-in” originated from the early days of corporate finance when companies issued stock to raise capital. Over time, the term “paid-in capital over par” was shortened to “additional paid-in capital.” On the other hand, the issue price is reflective of investor expectations of the company’s valuation. The difference between the par value and what the market thinks a share is worth determines the additional paid-in capital in the above equation. APIC is recorded at the initial public offering (IPO) only; the transactions that occur after the IPO do not increase the APIC account.

Paid-in Capital vs Retained Earnings

InnovateTech decides to raise capital by issuing shares of common stock to fund its growth and development. After attracting investors, InnovateTech successfully sells the shares at a price of $20.00 per share. Paid-in capital in excess of par also gives a company some flexibility when it comes to issuing new shares of stock. For example, if a company wants to issue new shares but doesn’t have enough cash on hand to cover the cost, it can use the paid-in capital to finance the issuance.

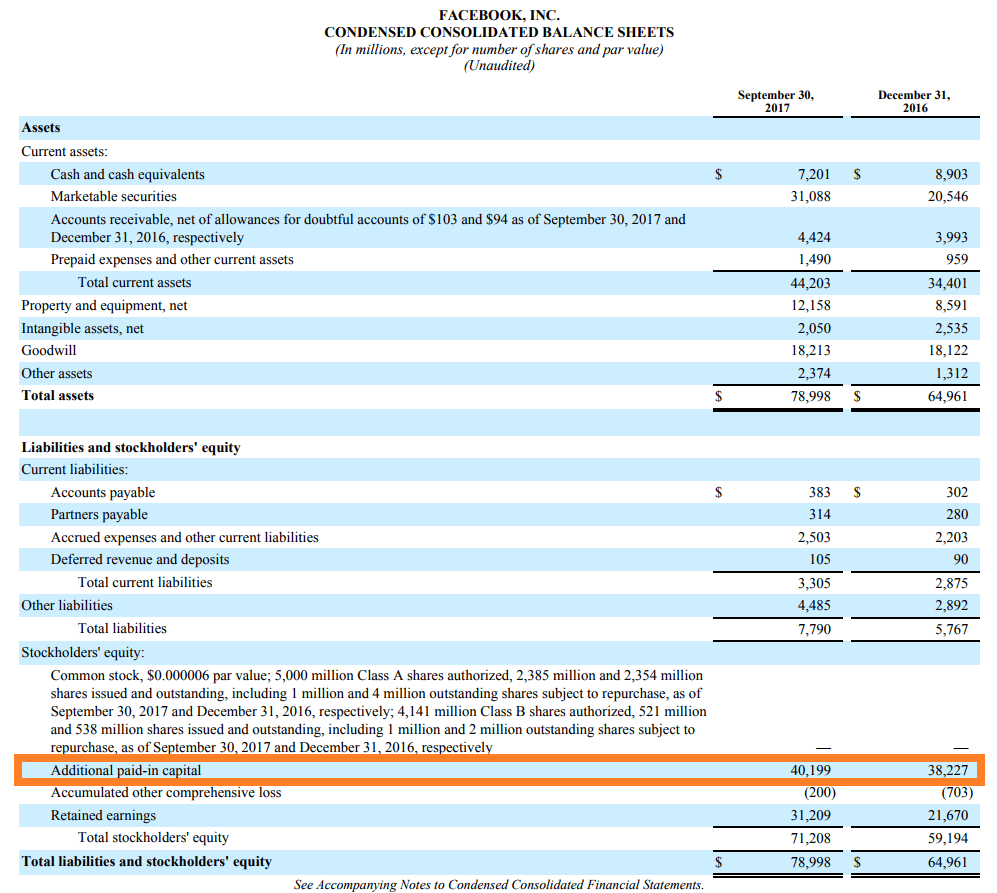

If preferred stock is sold instead of common stock, then a credit to the preferred stock account replaces the credit to the common stock account. Meanwhile, investors may elect to pay any amount above this declared par value of a share price, which generates the APIC. Upon multiplying the excess spread over the stated par value by the number of common shares outstanding, we arrive at an additional paid-in capital (APIC) value of $49.9 million.

- This capital provides a layer of defense against potential losses, in the event that retained earnings begin to show a deficit.

- – For example, if 1,000 shares of $10 par value common stock are issued by at a price of $12 per share, the additional paid-in capital is $2,000 (1,000 shares x $2).

- It is calculated by adding the par value of the issued shares with the amounts received in excess of the shares’ par value.

- A young company with big expectations might have significantly more paid-in capital than earned capital.

- Get stock recommendations, portfolio guidance, and more from The Motley Fool’s premium services.

- Paid-in capital includes the raised capital in excess of par value and what is raised at par value when a company sells preferred and common stock.

What does paid in capital account represent?

By raising capital through APIC, companies can improve their financial flexibility and reduce financial risk. Learn how additional paid-in capital is used to track equity fundraising contributions in a company. Let’s say Blue Star distributes a 5% bonus stock to its 2.0 million shareholders as a dividend. The buyback is frequently carried out when a corporation has significant financial reserves or surplus funds. Preferred stockholders have priority in receiving payment during bankruptcy proceedings.

Besides his extensive derivative trading expertise, Adam is an expert in economics and behavioral finance. Adam received his master’s in economics from The New School for Social Research and his Ph.D. from the University of Wisconsin-Madison in sociology. He currently researches and paid in capital in excess of par teaches economic sociology and the social studies of finance at the Hebrew University in Jerusalem. These materials were downloaded from PwC’s Viewpoint (viewpoint.pwc.com) under license. The amount to be received in the ordinary course of business in an arm’s length transaction.

But shareholders of the stock can resell them at a higher price to make profits. The retirement of treasury stock is also an option for the company if it doesn’t want to reissue it. Due to the retirement of treasury stock, the whole balance applicable to the number of retired shares gets reduced. Or the balance from the paid-in capital calculation at par value and the balance in additional share capital gets reduced accordingly depending on the number of retired treasury shares.

Companies may opt to remove treasury stock by retiring some treasury shares rather than reissuing them. The retirement of treasury stock reduces the balance of paid-in capital, applicable to the number of retired treasury shares. The balance sheet number on paid-in capital may reflect transactions in common shares, preferred shares, treasury stock, or some combination of all of these. Issuing Par Value Common Stock for Cash(assume par value is $1) dr. Cash $1.00cr. Common Stock $1.00to record issuance of 1 share of $1 par common stock if sold formore than par value (Assuming $5) dr. Cash $5cr. Common Stock $1Paid-in Capital in excess of par $4to record issuance of 1 share of common stock in excess ofpar.

The investors that participated in the capital raise paid $10.00 per common share. Although shares are rarely sold at par value, we will suppose that market participants have evaluated the stock to have a price of one dollar. It means that the par value of this stock is the same as its market value in the primary market. The price for which the stocks are initially sold is usually way above the par value.